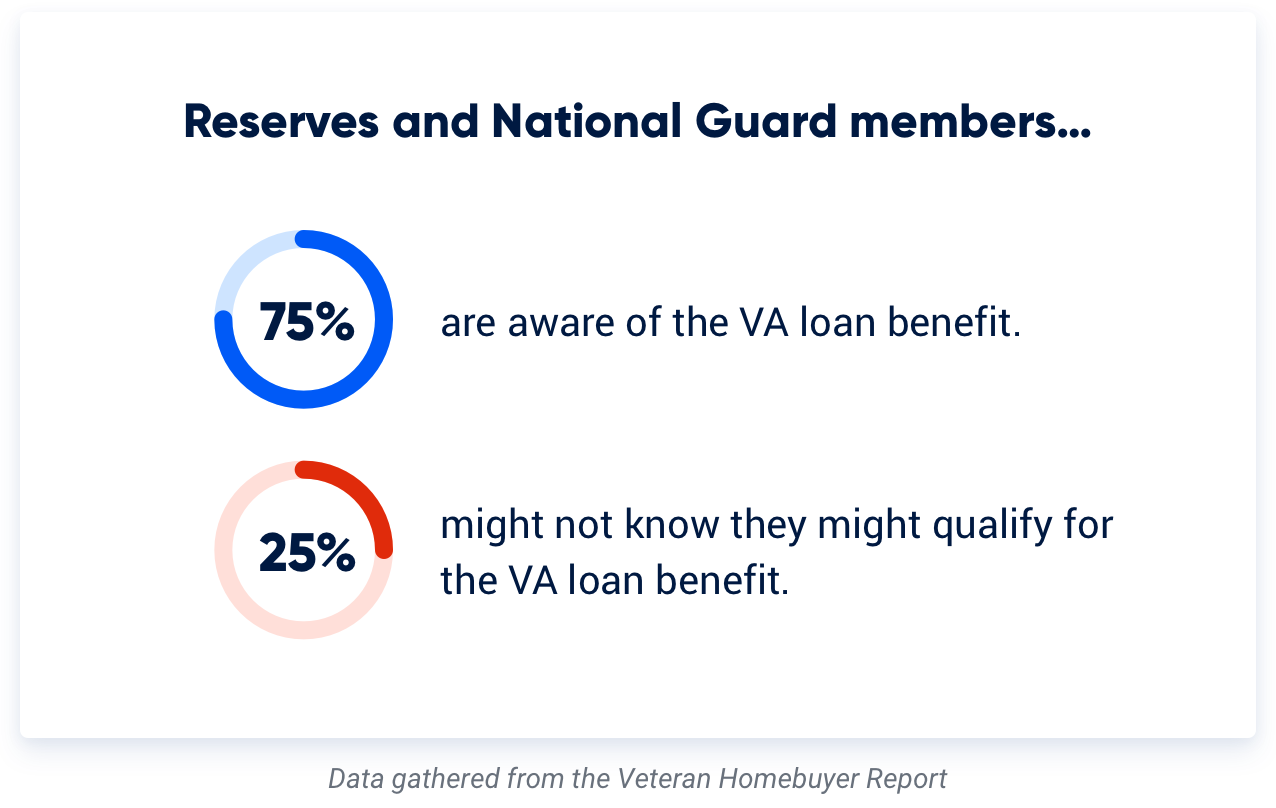

- National Guard and Reserve members can qualify for VA loans after serving for six years or fulfilling certain active-duty orders.

- A 2020 law expanded VA loan eligibility to more Guard members serving under Title 32 orders.

- Guard and Reserve borrowers are now issued Forms DD214 and DD214-1 to verify VA loan eligibility.

National Guard and Reserve members first gained access to the VA loan benefit in 1992. However, legislation passed in 2020 gave even more National Guard members access to VA loan benefits, including those on active duty.

Let's take a closer look at the VA loan requirements for National Guard and Reserve members, along with the latest changes that will make an estimated 50,000 more Guardsmen eligible for this historic home loan benefit.

Do National Guards or Reservists Qualify for VA Loans?

Yes, both National Guard and Reserve members may be eligible for VA loan benefits if they meet service requirements and were honorably discharged.

VA Loan Requirements for National Guard and Reserve

Generally, six years of service in the National Guard or Reserve is the catch-all requirement. Once you hit six years of honorable service, you're typically eligible for a VA loan.

There are also circumstances where it’s possible to earn VA home loan eligibility before six years. National Guard and Reserve members called to active duty service under Title 10 have gained VA loan eligibility for decades, as long as they serve at least 90 consecutive days.

Those who were discharged or released from active duty due to a service-connected disability prior to the six-year mark may also qualify. Guardsmen mobilized under Title 32 orders haven't had the same kind of early access to the VA loan benefit. That's where this new legislation makes a huge difference.

New Expanded VA Loan Eligibility for National Guard

VA loan eligibility for current and former National Guardsmen received a significant boost in 2020 thanks to the Veteran Health Care and Benefits Improvement Act.

This legislation helps bridge the eligibility gap between Title 10 and Title 32 service.

Now, National Guard members activated under Title 32 orders can be eligible for a VA loan after serving 90 cumulative days of full-time duty, of which at least 30 must have been consecutive.

The National Guard Association of the United States estimates that as many as 50,000 Guardsmen mobilized for the COVID-19 pandemic may gain immediate access to the home loan benefit.

This legislative change is also retroactive. National Guard members who served decades ago and now meet the new Title 32 guidelines could now be eligible for a VA loan.

VA Loan Documents for National Guard and Reserve

Some paperwork and documentation can vary, but the VA loan process isn't very different for National Guard or Reserve borrowers. They have access to the same significant homebuying benefits with the same general process.

Prospective homebuyers can talk with a Veterans United VA loan expert about their eligibility for the VA loan program. You don't need to have your Certificate of Eligibility in hand to start the VA mortgage process.

Once underway, lenders typically request service documentation. This may include:

- DD214 and DD214-1: The DD214-1, or Reserve Component Addendum, is a new document issued alongside the standard DD214 for National Guard and Reserve members. It combines all periods of service into one record, making it easier to verify eligibility and access VA benefits.

If you were discharged before this new form was implemented, you may still need to provide older documents, such as:

- NGB Form 22 and NGB Form 23 for National Guard members

- Points statement and discharge orders for Reservists

How Many Retirement Points Do I Need for a VA Loan?

Not counting active service or orders covered under the new law, essentially six "good" years' worth of points is needed for a VA home loan. A "good" year is a year with at least 50 retirement points.

Here’s a closer look at some service-specific documents lenders may also request:

- National Guard: NGB-22 or NGB-23

- Army Reserve: DARP Form FM 249-2E or ARPC Form 606-E

- Navy Reserve: NRPC 1070-124

- Air Force Reserve: AF 526

- Marine Corps Reserve: NAVMC HQ509 or NAVMC 798

- Coast Guard Reserve: CG 4174 or 4175

Counting National Guard and Reserve Income

Reserve and Guard homebuyers may be able to include their active service income when qualifying for a VA loan. As with other forms of effective income, stability and reliability are essential.

Lenders will look at your history of service and indications that it's likely to continue. If there are concerns about stability, lenders may at least be able to use that income to offset short-term obligations. In other words, your income from National Guard or Reserve service could cancel out other expenses expected to last a year or two.

Verification of continuance requires evidence of frequent service activations. In the absence of an activation history, the current orders must reflect a term of at least 12 months beyond the loan closing date to include the income in qualification calculations.

VA Funding Fee for National Guard and Reserve

Unless you have a service-connected disability or are a surviving spouse, all VA borrowers pay the VA Funding Fee. This fee goes directly to the Department of Veterans Affairs and helps keep the program going for future generations of service members and Veterans.

Before Jan 1, 2020, National Guard and Reserve members paid a higher VA Funding Fee. Under the Blue Water Navy Vietnam Veterans Act of 2019, the funding fee is now equal for all service types and only changes based on down payment and prior VA loan usage.

The VA Funding Fee is typically 2.15% or 3.3%, depending on the specifics of your loan. Use a VA Funding Fee calculator to figure out your fee, and keep in mind that it's possible to finance the VA Funding Fee into the loan or ask the seller to pay it.

Getting Started

The VA backs thousands of loans for National Guard and Reserve members and Veterans each year. With thousands of Guardsmen and Reservists now eligible for the VA loan, connect with a Veterans United VA loan expert online or call today at 855-870-8845 to learn more about your purchasing power.

How We Maintain Content Accuracy

Our mortgage experts continuously track industry trends, regulatory changes, and market conditions to keep our information accurate and relevant. We update our articles whenever new insights or updates become available to help you make informed homebuying and selling decisions.

Current Version

Apr 24, 2026

Written ByChris Birk

Reviewed ByTara Dometrorch

Updated article for DD214-1 documentation change. Content fact checked by team lead underwriter reviewer Tara Dometrorch.

Veterans United often cites authoritative third-party sources to provide context, verify claims, and ensure accuracy in our content. Our commitment to delivering clear, factual, and unbiased information guides every piece we publish. Learn more about our editorial standards and how we work to serve Veterans and military families with trust and transparency.

Related Posts

-

VA Renovation Loans for Rehab & Home ImprovementVA rehab and renovation loans are the VA's answer to an aging housing market in the United States. Here we dive into this unique loan type and the potential downsides accompanying them.

VA Renovation Loans for Rehab & Home ImprovementVA rehab and renovation loans are the VA's answer to an aging housing market in the United States. Here we dive into this unique loan type and the potential downsides accompanying them. -

Pros and Cons of VA LoansAs with any mortgage option, VA loans have pros and cons that you should be aware of before making a final decision. So let's take a closer look.

Pros and Cons of VA LoansAs with any mortgage option, VA loans have pros and cons that you should be aware of before making a final decision. So let's take a closer look.